|

GODINA/ YEAR: LI. ZAGREB,

20.

LISTOPADA 2014./ 20 OCTOBER, 2014 BROJ/

NUMBER: 12.1.3/2.

IZVJEŠĆE O

PREKOMJERNOME PRORAČUNSKOME MANJKU I RAZINI DUGA OPĆE DRŽAVE U REPUBLICI

HRVATSKOJ, LISTOPAD 2014. (ESA 2010)

EXCESSIVE DEFICIT PROCEDURE REPORT,

REPUBLIC OF CROATIA, OCTOBER 2014

(ESA 2010)

|

U ovom

priopćenju Državni zavod za statistiku objavljuje proračunski manjak

(deficit) i razinu duga opće države iskazane u Izvješću o prekomjernome

proračunskome manjku (deficitu) i razini duga opće države (listopadsko Izvješće)

za razdoblje 2010. – 2013. prema metodologiji Europskog sustava nacionalnih

i regionalnih računa (ESA 2010) i Priručniku o deficitu i dugu opće države.

|

|

The

Croatian Bureau of Statistics issues in this release the general government

deficit and debt data based on figures reported in the Excessive Deficit

Procedure Report (the October Notification) for the period from 2010 to

2013 according to the European System of National and Regional Accounts

(ESA 2010) methodology and the Manual on Government Deficit and Debt.

|

|

|

|

|

|

U

razdoblju od gotovo 20 godina, u kojem se primjenjivala ESA 95 kao

postojeći metodološki okvir za proizvodnju podataka nacionalnih računa,

gospodarstvo se znatno promijenilo, sa sve većom važnošću nematerijalne

imovine, proizvoda i usluga intelektualnog vlasništva te informacijskih i komunikacijskih

tehnologija u proizvodnim procesima. Iz tog je razloga bilo potrebno

prilagoditi i način kompiliranja makroekonomskih statistika kako bi i one

odražavale te promjene. Nastavno na to, od rujna 2014. sve zemlje Europske

unije obvezne su zamijeniti postojeći metodološki okvir ESA 95 novom

metodologijom ESA 2010. ESA 2010 europska je verzija svjetskog metodološkog

okvira Sustava nacionalnih računa (SNA 2008) Ujedinjenih naroda.

|

|

In the period of almost 20 years in which the ESA 95 has been

applied as methodological framework for producing national accounts data,

substantial changes impacted economies, particularly in relation to the

growing importance of intangible assets, intellectual property products and

services as well as of information and communication technologies in

production processes. Therefore, the way in which macroeconomic statistics

are compiled needed to be adjusted in order to reflect these changes.

According to this fact, since September 2014, all EU countries have been

obliged to replace the existing ESA 95 methodological framework with the

new ESA 2010 methodology. The ESA 2010 is the European version of the

System of National Accounts (SNA 2008) of the United Nations, a world-wide

methodological framework.

|

|

|

|

|

|

Fiskalni

nadzor Europske komisije nad zemljama članicama temelji se na Izvještaju o

prekomjernome proračunskome manjku i razini duga opće države. Ugovorom iz

Maastrichta uspostavljena su dva glavna kriterija fiskalnog nadzora: udio

proračunskog manjka (deficita) opće države zemlje članice ne smije biti

veći od 3% BDP-a, a konsolidirani dug opće države veći od 60% BDP-a.

|

|

The

fiscal surveillance of the European Union over the Member States is based

on the Excessive Deficit Procedure Report. The Maastricht Treaty defines

two main criteria of the fiscal surveillance: a deficit-to-GDP ratio and a

debt-to-GDP ratio must not exceed the reference values of 3% and 60%,

respectively.

|

|

|

|

|

|

Ovo

izvješće podnosi se Europskoj komisiji (Eurostat) dva puta godišnje – na

kraju ožujka (travanjsko Izvješće) i na kraju rujna (listopadsko Izvješće).

Izvješće se odnosi na razdoblje posljednje četiri godine i za tekuću

godinu, u kojoj su podaci za tekuću godinu bazirani na prognozama

Ministarstva financija. Nacionalni statistički uredi obvezni su objaviti

Izvješće na svojim internetskim stranicama.

|

|

This

EDP Report is submitted to the European Commission (Eurostat) twice a year

at the end of March (called the April Notification) and the end of

September (the October Notification). The EDP Report relates to a last

four-year period and for a current year in which current-year data are

based on the Ministry of Finance forecast. National statistical offices are

obliged to publish the EDP Report on their web sites.

|

|

|

|

|

|

Nastavno

na uvođenje nove metodologije ESA 2010 revidiran je i BDP te su se i iz tog

razloga izmijenili udjeli deficita i konsolidiranog duga opće države u

BDP-u u odnosu na travanjsku notifikaciju.

|

|

After

the introduction of the new ESA 2010, GDP has also been revised. Therefore,

compared with the April notification, the deficit and the consolidated

general government debt to GDP ratio was changed.

|

|

|

|

|

|

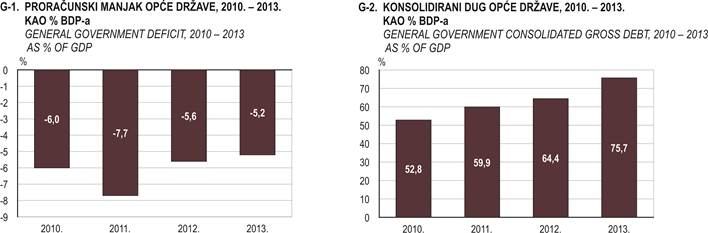

Primjenom

nove metodologije ESA 2010 deficit konsolidirane opće države za 2013.

iznosi -17 189 milijuna kuna, odnosno -5,2% BDP-a, dok za 2012. iznosi -18

654 milijuna kuna ili -5,6% BDP-a. Iz toga proizlazi da se u odnosu na

travanjsku notifikaciju deficit opće države u 2012. povećao za 2 366

milijuna kuna, dok se u 2013. povećao za 1 017 milijuna kuna. Također

u odnosu na travanjsku notifikaciju, u 2010. se godini deficit smanjio za

769 milijuna kuna, a u 2011. za 265 milijuna kuna.

|

|

With

the implementation of the new ESA 2010 methodology, the general government

deficit for 2013 was estimated at -17 189 million kuna, or -5.2% of GDP,

while for 2012 it was estimated at -18 654 million kuna, or -5.6% of

GDP. Consequently, in comparison with the April notification, the annual

deficit increased by 2 366 million kuna in 2012 and by 1 017 million kuna

in 2013. Furthermore, the annual deficit decreased by 769 million kuna in

2010 and by 265 million kuna in 2011, compared with the April notification.

|

|

|

|

|

|

Najveći

utjecaj na povećanje deficita za 2013., u odnosu na travanjsku

notifikaciju, imalo je uključivanje Hrvatskih autocesta i Autoceste Rijeka –

Zagreb u obuhvat opće države (u iznosu od 337 milijuna kuna), kao i

revizija bruto investicija u fiksni kapital (u iznosu od 461 milijun kuna).

|

|

In

comparison with the April notification, the inclusion of Hrvatske Autoceste

d. o. o. and the Rijeka-Zagreb Motorway in the coverage of the general

government sector (in the amount of 337 million kuna) as well as revision

of gross fixed capital formation (in the amount of 461 million kuna) had

the most significant effect on the deficit increase.

|

|

|

|

|

|

Također, na prihodnoj strani važno je spomenuti

reviziju poreznih prihoda. Najvažniji dio revizije o porezima odnosi se na

promjenu koncepta poreznih prihoda te na primjenu posebnih smjernica

Eurostata, što je rezultiralo dopunom liste prihoda koji se smatraju porezima.

Tako je lista poreznih prihoda dopunjena premijama osiguranja depozita

Državne agencije za sanaciju banaka i osiguranje štednih uloga te s

nekoliko poreza na lutriju, igre na sreću i oklade. No ukupna revizija

poreza nije znatno utjecala na smanjenje deficita jer je najvažnija stavka

povećanja poreznih prihoda, premija osiguranja depozita, ujedno povećala

rashode za isti iznos (kroz kategoriju plaćenih tekućih transfera) te je njen utjecaj na deficit jednak nuli.

Nadalje, udio prihoda od PDV-a koji zemlje članice uplaćuju u proračun

EU-a, prema metodologiji ESA 2010, više se ne prikazuje zasebno, nego se

uključuje u ukupne prihode od PDV-a zemlje članice. S druge se strane, u

obliku raznih tekućih transfera, za isti iznos ujedno povećava rashodna strana

te je utjecaj te stavke na deficit jednak nuli.

|

|

Moreover, on the revenue side, it is important to

stress out the revision of tax revenues. The most important part of the tax

revision is related to a change of the concepts of tax revenues and to the

implementation of specific Eurostat's guidelines, which resulted in the

extension of the list of revenues by adding those that are considered

taxes. Therefore, the list of tax revenues has been supplemented with the

deposit insurance premiums of the State Agency for Deposit Insurance and

Bank Rehabilitation and with several taxes on lottery, gambling and

betting. However, the overall tax revision did not have a significant

impact on the reduction of deficit, since the most important item that

contributes to the increase of tax revenues, the deposit insurance premium,

increased the expenditures by the same amount (through the category of

current transfers payable) at the same time, thus its impact on the deficit

was zero. Furthermore, the VAT contribution to the EU budget

paid by the Member States, according to the ESA 2010 methodology, is not

shown separately any more, but is included in the total VAT revenues of a

particular Member State. On the other hand, it increased the expenditure

side in the form of miscellaneous

current transfers, thus its impact on the deficit was zero.

|

|

|

|

|

|

Primarni deficit opće države u 2013. iznosio je -6 086 milijuna kuna

ili

-1,8% BDP-a, dok je u 2012. iznosio -7 875 milijuna kuna ili -2,4% BDP-a.

|

|

The primary

general government deficit in 2013 was -6 086 million kuna, or -1.8% of

GDP, while in 2012 it was -7 875 million kuna, or

-2.4% of GDP.

|

|

|

|

|

|

Primjenom

nove metodologije ESA 2010 za razdoblje od 2010. do 2013. konsolidirani je

dug opće države u prosjeku porastao za 27 do 29 milijardi kuna godišnje.

Tako u 2012. iznosi 212 964 milijuna kuna ili 64,4% BDP-a, a u 2013. godini

249 836 milijuna kuna ili 75,7% BDP-a. Dug opće države promijenio se

isključivo zbog povećanja obuhvata podsektora središnje države, čime su

primljeni krediti tih jedinica ušli u obuhvat duga.

|

|

With

the implementation of the new ESA 2010 methodology for the period from 2010

to 2013, the consolidated gross debt of the general government increased on

the average by 27 to 29 billion kuna, that is, in 2012 it amounted to 212

964 million kuna, or 64.4% of GDP, and in 2013 to 249 836 million kuna, or

75.7% of GDP. The general government debt changed exclusively due to the

expansion of the central government subsector coverage, which resulted with

the inclusion of the received loans of these units into the debt.

|

|

|

|

|

|

Prema

projekcijama Ministarstva financija, proračunski saldo državnog proračuna u

2014. iznosit će -19 010 milijuna kuna ili -5,8% BDP-a, a konsolidirani dug

opće države na kraju godine 268 568 milijuna kuna ili 81,8% BDP-a.

|

|

According

to the Ministry of Finance forecast, the deficit in 2014 will amount to -19

010 million kuna, or -5.8% of GDP, and the consolidated gross debt of the

general government at the end of the year to 268 568 million kuna, or 81.8%

of GDP.

|

|

|

|

|

|

|

|

|

|

Podatke

iz ovog priopćenja možete preuzeti na

www.dzs.hr.

Ovdje

možete

preuzeti

EDP tablice

iz

ovog

priopćenja

u excel

formatu.

Ovdje

možete

preuzeti

tablicu

temeljnih agregata sektora opće države

u excel

formatu.

|

|

Data from this release can be downloaded at www.dzs.hr.

EDP Excel

tables from this Release can be downloaded here

Excel table with data on main aggregates of general government from this release can be downloaded here

|

1. PRIKAZ PREKOMJERNOGA PRORAČUNSKOG MANJKA I

RAZINE DUGA TE POVEZANIH PODATAKA

REPORTING

OF EXCESIVE GOVERNMENT DEFICIT AND DEBT LEVELS AND PROVISION OF ASSOCIATED

DATA

|

|

2010.

|

2011.

|

2012.

|

2013.

|

|

|

mil. kuna

Mln

kuna

|

%

|

mil. kuna

Mln

kuna

|

%

|

mil. kuna

Mln

kuna

|

%

|

mil. kuna

Mln

kuna

|

%

|

|

|

|

|

|

|

|

|

|

|

|

Bruto domaći proizvod, tekuće tržišne cijene

Gross domestic product at current market prices

|

328

041

|

100,0

|

332

587

|

100,0

|

330

456

|

100,0

|

330

135

|

100,0

|

|

|

|

|

|

Neto

uzajmljivanje (-)/neto pozajmljivanje (+)

Net

borrowing (-)/net lending (+)

|

|

|

|

|

|

|

|

|

|

|

|

Opća država

General government

|

-19

795

|

-6,0

|

-25

494

|

-7,7

|

-18

654

|

-5,6

|

-17

189

|

-5,2

|

|

Središnja država

Central government

|

-19

682

|

-6,0

|

-24

862

|

-7,5

|

-17

759

|

-5,4

|

-18

760

|

-5,7

|

|

Lokalna

država

Local government

|

-31

|

0,0

|

-220

|

-0,1

|

210

|

0,1

|

76

|

0,0

|

|

Fondovi

socijalne sigurnosti

Social security funds

|

-81

|

0,0

|

-412

|

-0,1

|

-1

105

|

-0,3

|

1

496

|

0,5

|

|

|

|

|

|

Konsolidirani

dug opće države

General

government consolidated gross debt

|

|

|

|

|

|

|

|

|

|

|

|

Opća država

General government

|

173

087

|

52,8

|

199

311

|

59,9

|

212

964

|

64,4

|

249

836

|

75,7

|

|

|

|

|

|

Rashodi

opće države

General

government expenditure

|

|

|

|

|

|

|

|

|

|

|

|

Bruto investicije u fiksni kapital

Gross fixed capital formation

|

10

745

|

3,3

|

11

659

|

3,5

|

11

699

|

3,5

|

10

964

|

3,3

|

|

Kamate (konsolidirano)

Interest (consolidated)

|

7

773

|

2,4

|

9

690

|

2,9

|

10

779

|

3,3

|

11

102

|

3,4

|

2. REVIZIJA PREKOMJERNOGA PRORAČUNSKOG MANJKA

I RAZINE DUGA

REVISION

OF EXCESIVE GOVERNMENT DEFICIT AND DEBT LEVELS

|

|

2010.

|

2011.

|

2012.

|

2013.

|

|

|

mil. kuna

Mln kuna

|

%

|

mil. kuna

Mln kuna

|

%

|

mil. kuna

Mln kuna

|

%

|

mil. kuna

Mln kuna

|

%

|

|

|

|

|

|

|

|

|

|

|

|

Neto

uzajmljivanje (-)/neto pozajmljivanje (+)

Net borrowing (-)/net lending (+)

|

|

|

|

|

|

|

|

|

|

Prije revizije

Before revision

|

-20 564

|

-6,4

|

-25 759

|

-7,8

|

-16 288

|

-5,0

|

-16 172

|

-4,9

|

|

Poslije revizije

After revision

|

-19 795

|

-6,0

|

-25 494

|

-7,7

|

-18 654

|

-5,6

|

-17 189

|

-5,2

|

|

Razlika

Difference

|

769

|

0,3

|

265

|

0,2

|

-2 366

|

-0,7

|

-1 017

|

-0,3

|

|

|

|

|

|

|

|

|

|

|

|

Konsolidirani

dug opće države

General government consolidated gross debt

|

|

|

|

|

|

|

|

|

|

Prije revizije

Before revision

|

145 721

|

45,0

|

170 859

|

52,0

|

183 676

|

55,9

|

220 196

|

67,1

|

|

Poslije revizije

After revision

|

173 087

|

52,8

|

199 311

|

59,9

|

212 964

|

64,4

|

249 836

|

75,7

|

|

Razlika

Difference

|

27 366

|

7,8

|

28 452

|

8,0

|

29 288

|

8,5

|

29 640

|

8,6

|

|

METODOLOŠKA OBJAŠNJENJA

|

|

NOTES ON METHODOLOGY

|

|

|

|

|

|

|

|

|

|

Osnovni

pojmovi i definicije

|

|

Basic concepts and definitions

|

|

|

|

|

|

Sektor

opće države (S.13) uključuje sve institucionalne jedinice koje su ostali

netržišni proizvođači, čiji je output namijenjen individualnoj i

zajedničkoj potrošnji, te se uglavnom financira od obveznih uplata jedinica

koje pripadaju drugim sektorima i/ili svih institucionalnih jedinica koje

su ponajprije uključene u preraspodjelu nacionalnog dohotka i bogatstva.

|

|

The general

government sector (S.13) includes all institutional units that are other

non-market producers, whose output is intended for individual and

collective consumption and mainly financed by compulsory payments made by

units belonging to other sectors and/or all institutional units principally

engaged in the redistribution of national income and wealth.

|

|

|

|

|

|

Sektor opće države sastoji se od tri podsektora:

središnje države (S.1311), lokalne države (S.1313) i fondova socijalnog

osiguranja (S.1314). Središnja država obuhvaća državne upravne

organizacije, državne agencije te ostale vladine institucije koje imaju

nadležnost nad cijelim gospodarskim teritorijem te su odvojene od fondova

socijalne sigurnosti. Središnja država uključuje i neprofitne institucije

koje su pod kontrolom i uglavnom ih financira središnja vlast. Središnja

država u ovome fiskalnom izvješću obuhvaća korisnike državnog proračuna,

izvanproračunske korisnike (Hrvatske vode, Fond za zaštitu okoliša i

energetsku učinkovitost, Hrvatske ceste, Hrvatski fond za privatizaciju do

31. ožujka 2011., Agenciju za upravljanje državnom imovinom do 30. rujna

2013., Centar za restrukturiranje i prodaju te Državni ured za upravljanje

državnom imovinom kao njezinih pravnih sljednika) zajedno s HŽ

Infrastrukturom, HRT-om, Hrvatskim autocestama i Autocestom Rijeka ‒ Zagreb, koji su

reklasificirani u sektor države (središnje države).

|

|

The general government consists of three sub-sectors:

the central government (S.1311), the local government (S.1313) and the

social security funds sub-sector (S.1314). The central government comprises

departments of government administration and other central government

agencies, authorities and institutions whose jurisdiction covers the entire

economic territory, apart from the administration of the social security

funds sub-sector. It also includes non-profit institutions that are

controlled and chiefly financed by the central government. The central

government in this EDP Report includes central government budgetary users,

extra-budgetary users (the Croatian Waters, the Fund for Environmental

Protection and Energy Efficiency, the Croatian Roads, the Croatian

Privatization Fund until 31 March 2011, the Agency for Management of the

Public Property until 30 September 2013, that is, the Restructuring and Sale Center and the State

Property Management Administration as its legal successors) together with

the Croatian Railways Infrastructure, the Croatian Radio and Television, Hrvatske

Autoceste d. o. o. and the Rijeka-Zagreb Motorway which have been

reclassified into the government sector (the central government).

|

|

|

|

|

|

Lokalna

država obuhvaća jedinice lokalne i područne samouprave te sve korisnike

lokalnih proračuna. Uključuje i neprofitne institucije koje su pod

kontrolom lokalne vlasti i uglavnom ih ona financira. Podsektor fondova

socijalne sigurnosti uključuje sve institucionalne jedinice čija je

primarna djelatnost administracija sustava socijalne sigurnosti. Stoga taj

sektor čine Hrvatski zavod za zdravstveno osiguranje, Hrvatski zavod za

mirovinsko osiguranje i Hrvatski zavod za zapošljavanje.

|

|

The

local government sector comprises local and regional self-government units

as well as all local budget users. Included in the local government sector

are also non-profit institutions controlled and chiefly financed by local

authorities. The social security funds sub-sector includes all public

sector institutional units whose main activity consists in administrating

funded social insurance systems. Therefore, it consists of the Croatian

Health Insurance Fund, the Croatian Institute for Pension Insurance and the

Croatian Employment Institute.

|

|

|

|

|

|

Proračunski

manjak (višak) znači neto uzajmljivanje/neto pozajmljivanje (EDP B.9)

sektora opće države (S.13) odnosno razliku između ukupnih prihoda i ukupnih

rashoda, kako je definirano u ESA 2010.

|

|

The

government deficit (surplus) means the net borrowing/net lending (EDP B.9)

of the general government sector (S.13) defined as a difference between a

total revenue and a total expenditure.

|

|

|

|

|

|

Prema

novoj metodologiji ESA 2010 nema više prilagodbi za tretman tijekova kamata

iz swap ugovora i sporazuma o terminskom tečaju, tako da su EDP B.9

i B.9 prema metodologiji ESA 2010 jednaki.

|

|

According

to the new ESA 2010 methodology, no further adjustments are made in the

treatment of the interest calculation of flows relating to swaps and

forward rate agreements, which means that EDP B.9 is now aligned with B.9

according to the ESA 2010.

|

|

|

|

|

|

Dug

opće države predstavlja bruto nominalnu vrijednost duga na kraju godine.

Dug se odnosi na jedinice klasificirane prema službenoj sektorskoj

klasifikaciji u sektor opće države (S.13), a čine ga sljedeći financijski

instrumenti: gotovina i depoziti (AF.2); dužnički vrijednosni papiri (AF.3)

te krediti i zajmovi (AF.4), kako je definirano u ESA 2010.

|

|

The general government debt is defined as gross debt

nominal value at the year end. The debt refers to the units classified in

the general government sector (S.13) according to the sector classification

and consists of the following financial instruments: currency and deposits

(AF.2), debt securities (AF.3) and loans (AF.4), as defined in the ESA

2010.

|

|

|

|

|

|

|

|

|

|

Kratice

|

|

Abbreviations

|

|

|

|

|

|

BDP

|

bruto domaći

proizvod

|

|

EDP

|

excessive deficit

procedure

|

|

EDP

|

postupak

prekomjernog deficita

|

|

ESA

|

European System of

Accounts

|

|

ESA

|

Europski sustav

nacionalnih računa

|

|

EU

|

European Union

|

|

EU

|

Europska unija

|

|

GDP

|

gross domestic

product

|

|

HRT

|

Hrvatska

radiotelevizija

|

|

mln

|

million

|

|

HŽ

|

Hrvatske

željeznice

|

|

VAT

|

value added tax

|

|

mil.

|

milijun

|

|

|

|

|

PDV

|

porez na dodanu

vrijednost

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Objavljuje

i tiska Državni zavod za statistiku Republike Hrvatske, Zagreb, Ilica 3, p.

p. 80.

Published and printed by the Croatian Bureau of Statistics, Zagreb,

Ilica 3, P. O. B. 80

Telefon/ Phone:

+385 (0) 1 4806-111, telefaks/ Fax: +385 (0) 1 4817-666

Odgovara

ravnatelj Marko Krištof.

Person

responsible: Marko Krištof, Director General

Priredile:

Galjinka Dominić, Valentina Hudiluk, Marija Gojević, Ana-Marija Kolić i Suzana

Šimičić

Prepared

by: Galjinka

Dominić, Valentina Hudiluk, Marija Gojević, Ana-Marija Kolić and Suzana

Šimičić

|

|

MOLIMO

KORISNIKE DA PRI KORIŠTENJU PODATAKA NAVEDU IZVOR.

USERS

ARE KINDLY REQUESTED TO STATE THE SOURCE

|

|

Naklada:

20 primjeraka

20 copies

printed

Podaci iz

ovog priopćenja objavljuju se i na internetu.

First

Release data are also published on the Internet.

|